Driving Financial Inclusion with Sales Intelligence

Banking started before 2000 BCE. Lending began with merchants giving grain loans to farmers, and archaeology even shows the reference to money lending in Ancient times.

But what evidence would future archaeologists of the next century get when they dig into the banking history of the 21st century?

Credit has always been an instrument to increase the financial capacity of an entity by providing them the wallet share to buy goods and services, which subsequently facilitates economic growth. The economic growth dependent on credit demands more volume of credit disbursed, which lets people progressively purchase goods and services; that align with a nation’s financial inclusion requirements.

Financial inclusion makes financial and banking services more accessible, convenient, and affordable for maximal demography. Until 2020-21, Govt. of India could only disburse 1.47 lakh crore to 45 lakhs MSMEs (which have Bank/credit history), while the initial goal was to disburse 3 lakh crore to MSMEs. It has been the priority for the government and BFSI sector to increase the number of entities opening bank accounts and accessing credit.

Remember Sharma Ji? Sharma Ji was a Mizoram-based merchant and happy-go-lucky with his business. Being a small-time merchant, Sharma Ji never planned his business in terms of growth and management and was primitive with his strategies; neither he had a bank account or billing system. July 2022 went a little rough for him, as he had only done business in cash, and with the Indian economy evolving, there was a high demand for UPI as a mode of payment by customers.

Sharma Ji never went to a bank, and there is a considerable gap in understanding how to open a bank account and implement UPI. Not only was there competition and a change in the mode of payments, but there was a significant requirement for Sharmaji to access credit and grow his business.

Previously, we also came across Rahul, the local branch manager from Motak Bank, working on a similar problem. Rahul came across the fact that the majority of merchants like Sharma Ji, who is NTB and NTC, are dealing in cash transactions and are not even visible to the bank. He struggled while disbursing loans and onboarding new merchants, where he faced challenges like

- Low Depth Information

- Visibility into New-to-bank (NTB) Customers

- Hostility while lending to New-to-credit (NTC) Customers

While Rahul could use alternative data to disburse more loans, his performance came to notice to Manish Gaurav, the sales head at Motak. Motak Bank became a part of RBI’s Vision for financial inclusion and aligned with the principles. They were to identify new opportunities, and as the sales head, Manish was to make sure that:

- Adequate infrastructure is available in rural regions to increase the volume of digital transactions.

- Onboarding New to credit and New to bank merchants with intent and stability to repay.

But before the issue of increasing the number of loans disbursed comes into the picture, banks need to consider that many such Sharma Ji(s) do not even have basic bank accounts, leading to them not having access to financial services like POS & UPI, that would help them be more visible in terms of credit. And also help them manage/ record business transactions easily.

Why is UPI important for merchants? Given the smartphone penetration & the volume of UPI transactions in regions like Sharma Ji’s vicinity, people are well versed with this payment method and probably prefer UPI more than cash.

Hence, Sharma Ji getting access to UPI would also lead to increased business daily.

Traditionally going through this intricate process of studying these untapped demographics and coming up with a strategy to distribute financial services in these regions gets complicated due to the redundant and diverse data available to them. But given the involvement of AI and ML present day, and despite the increased amount of digital transactions, why does financial inclusion still seem impracticable in some regions?

What’s the gap?

Alternative Data and data such as the new oil have been able to innovate the ancient system. Sharmaji being from India’s largest unorganized sector, i.e., Retail, initially didn’t get much visibility in the bank’s potential lending list. After using alternative data, the bank manager could profile Sharmaji based on Data Sutram’s parameters, got enhanced visibility and was able to onboard him with a new bank account. With this, Data Sutram helps them create a scorecard that helps them get a loan. As Sharma Ji was able to get his loan sanctioned by the banks, there have been various challenges for the Financial Institutions to reach felicitous regions or extract similar desirable results. Helping more people from untapped and rural areas has multiple barriers due to more cash transactions and the unavailability of mobile networks in these regions. And there are specific questions around it:

- How do we identify remote opportunities that are void of digital footprint?

- Are the new opportunities being identified efficiently, or is there a missing piece in the puzzle?

- Are the existing opportunities being used to their full potential?

- Do we know the entity we are selling?

Pondering upon these questions, we understand why the sales aren’t performing, giving the desired results.

That brings us back to how we can facilitate all of this.

What’s the solution?

The above questions and the quest for their answers all boil down to Where, How and Who?

Financial inclusion is based around.

- Where should we start or identify the untapped region

- How do we enhance the potential of existing opportunities

- And, Who still needs to be financially included?

What’s the solution?

The above questions and the quest for their answers all boil down to Where, How and Who?

Financial inclusion is based around.

- Where should we start or identify the untapped region

- How do we enhance the potential of existing opportunities

- And, Who still needs to be financially included?

The omnipresence of alternative data with different use cases has been very evident but does it help sell financial services?

To begin with this financial inclusion, banks need first to approach merchants to open bank accounts-just like how the Motak bank representative is doing for Sharmaji, giving them access to POS & UPI, thus making them take the first step towards being credit active.

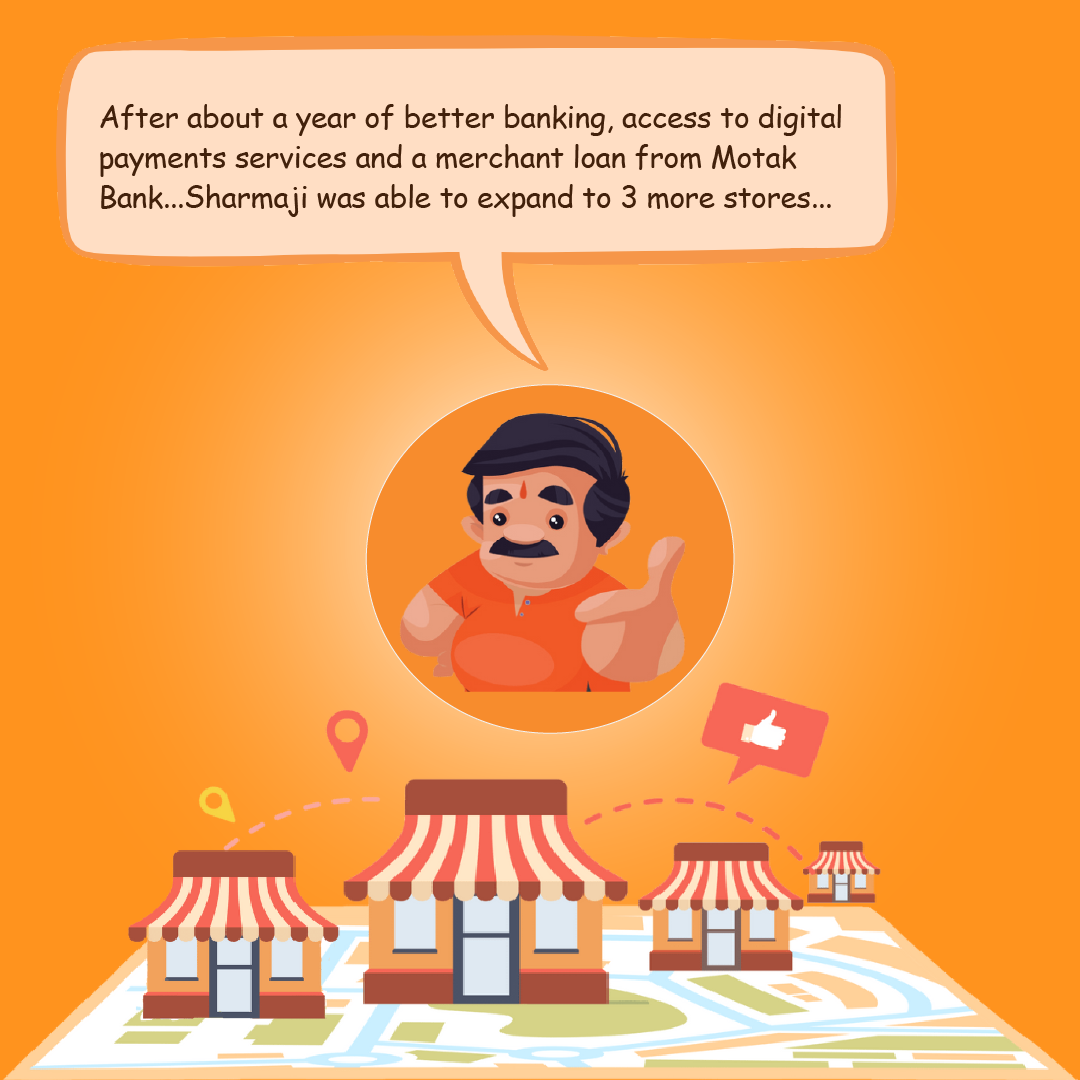

For merchants like Sharma Ji, financial inclusion helps them log their business transactions and apply for a loan with the representative’s assistance after some time. This gives them room to plan his growth in nearby areas where he may want to set up shops or invest in increasing his current product range. However, Sharamji plans to scale his business.

And answering the above question, yes, it does; this all becomes part of the Sales Intelligence. Financial services are fundamental, but sometimes the solutions aren’t.

What is Sales Intelligence?

As the term suggests, Sales Intelligence is getting complete visibility into different levels of geography, using alternative data to derive actionable insights from 250+ sources. Financial services in rural regions aren’t difficult to initiate. Still, it’s always a challenge to identify if the location needs that service.

Under the purview of Data Sutram’s parameters, Financial Institutions get a better insight into granular and macro-level information about the geographies they wish to target.

Sharmaji and other merchants from the sector often go unseen, as it is one of the largest unorganized sectors in terms of data. Not only does sales intelligence provide visibility of such entities, it even helps NTB/NTC customers like Sharma Ji access better financial services.

Sales Intelligence provides a solution that organizes various data parameters that help financial institutions with catchment-level data parameters, such as

- SME & MSME Density

- Economic Activity

- Delinquency Rates

- Card/UPI Usage

- Loan Disbursement Trends

- Income & Affluence

- Transaction Volumes

And several other parameters help them know which merchant to onboard, in which area and resource & product planning to expedite financial inclusion.

This helps various stakeholders just like Manish and his team, from banks, NBFCs, and fintech with

- Branch Analysis

- Estimate of the revenue opportunities in the target locations

- Planning and allocation of budgets for effective targeting

- Sales Positioning

- Planning of human resources

- Beat planning

- Lead generation

- Merchant Verification & Profiling for Lending & Cross-Selling

Conclusion

Data Sutram’s Sales Intelligence helps financial Institutions get a panorama of merchant data, location data and consumer data, which allows them to identify where, how and who at the macro and branch levels.

Using Data Sutram’s Sales Intelligence, Manish and Motak Bank were able to onboard NTC customers from unutilized regions. It provided adequate infrastructure for Safe, Secure, Fast, Convenient, Accessible, and Affordable financial solutions.

Empowered by this Sales Intelligence, merchants like Sharma Ji got new bank accounts and access to credit and could scale their business. And subsequently, providing data visibility into an entirely unorganized sector fuels the financial inclusion wagon, onboarding nearly half a billion invisible to credit customers.

With these solutions, Data Sutram is aligned with the government and RBI’s vision of financial inclusion aiding businesses, FinTechs, and payment providers to be part of this mission. Our Sales Intelligence generated from alternative data sources help Increased Bank Account Opening, Increase UPI & POS Adoption, Increased Loan Disbursements and be intrinsic to the vision.